Research | April 2026

Fluvial inundation in Seville: Climate trends, insurance gap and granularity challenge

Alpha-Klima has conducted an analysis on the impact of riverine inundation along the Spanish city of Seville. The study focuses on postcode-level risk distribution, combining forward-looking flood hazard data with exposure and vulnerability modelling to assess potential impacts on insurance portfolios.

Key insights

- Forward-looking, postcode-level fluvial flood risk analysis for Seville's residential stock

- Climate trends could materially shift claims patterns beyond what historical data captures

- Granular methodology: hazard, vulnerability and exposure modelling adapted to insurance-portfolio data

- The insurance gap persists in Spain even with the Consorcio de Compensación de Seguros — measuring risk evolution matters more than ever

The challenge for insurers

Fluvial flood risk is already one of the most impactful physical risks in Europe, and a growing body of evidence suggests that its impact could intensify over the coming decades. In Spain, public authorities explicitly recognize climate change as «one of the factors contributing to an increase in both the probability of flood occurrence and its negative impacts.»

For the insurance sector, this means that flood risk can no longer be analysed solely through the lens of historical events. It is increasingly a question of whether historical claims data, however useful it remains, still provides a sufficient basis for understanding the risk profile of today’s portfolios and supporting tomorrow’s underwriting decisions. The implication is straightforward: historical claims experience continues to be valuable, but on its own it may not fully capture how flood frequency, severity and spatial distribution evolve under changing climate conditions.

These trends create a growing challenge for insurers across Europe. In 2023, the German Insurance Association (GDV) published an article highlighting that rising climate-related claims costs could materially increase property insurance premiums over the next decade, with some scenarios pointing to a potential doubling. This is compounded by EIOPA’s concern that, in highly exposed areas, coverage against natural catastrophes may become increasingly difficult to maintain in terms of both availability and affordability.

Seville as a case in point

In this context, Seville represents a particularly relevant and timely case. In February 2026, storm Leonardo caused the Guadalquivir River to overflow in several areas of Andalusia, forcing the evacuation of thousands of people and highlighting the exposure of certain locations to flood risk.

This is further reinforced by the fact that Seville stands out among major Spanish cities in terms of potential exposure to flooding. Various estimates suggest that a significant share of its residential stock could be affected by high return-period flood events, underlining the need for more granular and forward-looking risk assessment.

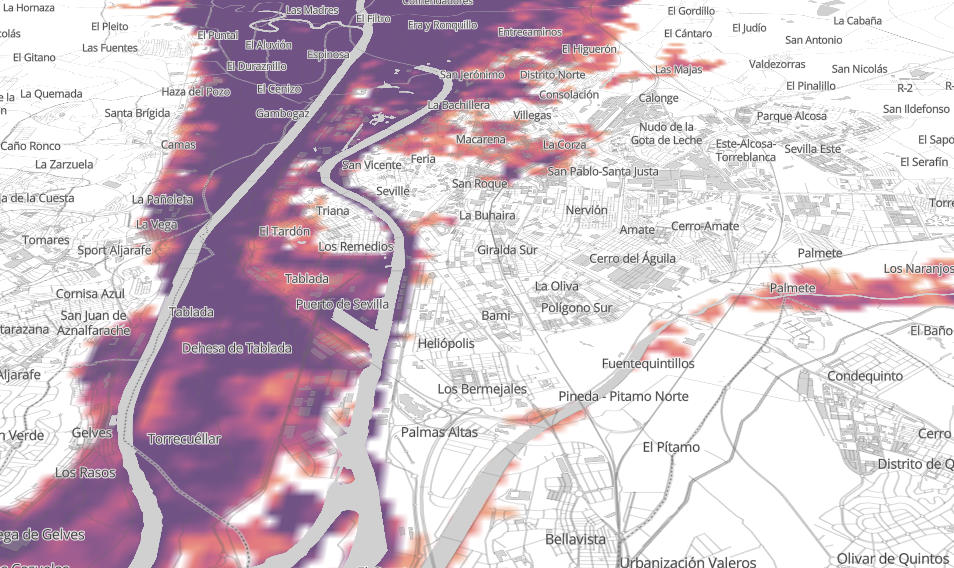

The figure below shows an example of the flood risk map available in the Alpha-Klima platform for the Seville area. The high spatial resolution of the underlying data, combined with asset-specific vulnerability models, allows moving beyond a purely geographic view of risk towards a quantification of potential impacts, both at individual asset level and across insurance portfolios exposed to the city.

Data limitations

However, insurers do not always have access to precise geolocation data for their exposures, nor is this information consistently structured, clean and homogeneous across their systems. This limitation is not trivial, as the quality and granularity of exposure data directly constrain the ability to assess physical risk in a robust and decision-relevant way.

A practical way to address this challenge is to align the level of risk analysis with the actual resolution of the available exposure data. In this context, aggregating geographic information, for example at postcode level, provides a pragmatic starting point. It enables insurers to build an initial layer of territorial prioritisation and accumulation analysis, identify concentrations of exposure, and highlight areas where a more detailed assessment is warranted.

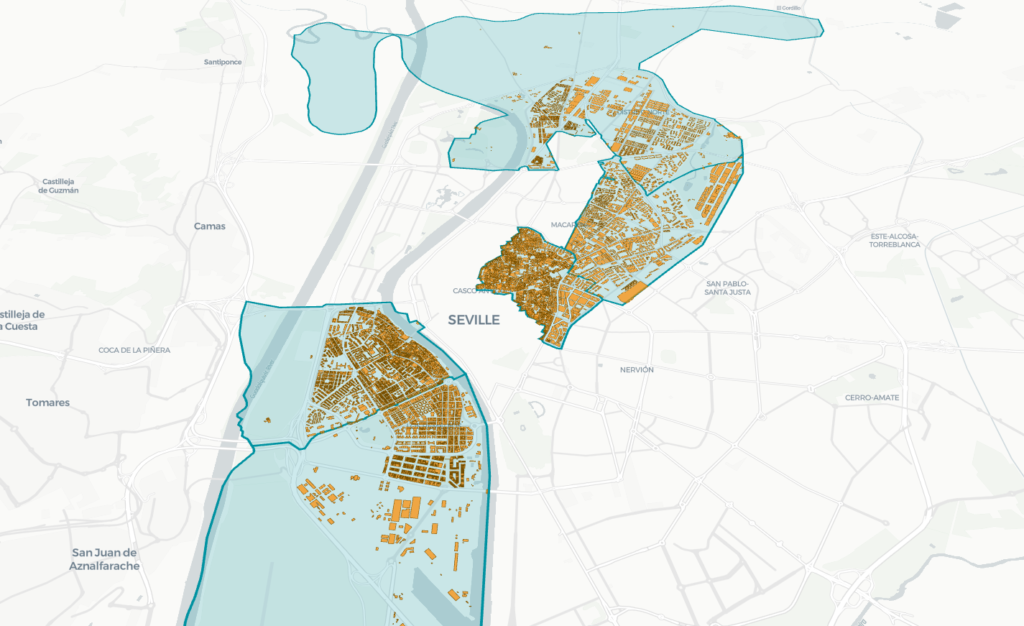

By combining building geolocation data from OpenStreetMap with market price data per square metre across different areas of Seville [1], it is possible to construct a first-order estimate of exposure value to flood risk at postcode level. This approach allows geospatial and market data to be translated into an aggregated exposure proxy that is consistent with the type of information typically available in insurance portfolios. The map below shows the five postcodes with the highest estimated exposure to flood risk in the city of Seville.

[1] Market price data was obtained from Idealista.

One of the most relevant findings is that certain postcodes in the historic city centre (41003) and the Macarena district (41008) exhibit higher levels of exposure than other postcodes located closer to the river. This highlights the importance of considering not only proximity to the hazard, but also the topography of the place and the distribution and value of exposed assets, which can significantly alter the interpretation of risk from an insurance perspective.

From a forward-looking perspective, the analysis also evaluates how the Solvency Capital Requirement (SCR) associated with these exposures could evolve up to 2035 under an unfavourable climate scenario (Hot-House-World). The table below presents the results for the five most exposed postcodes.

The methodological approach incorporates physical factors such as river basin topography, which influences the propagation and accumulation of flood waters, as well as the spatial correlation structure of flood risk. Risk aggregation is performed using copula-based techniques, applied to reflect effective full level of dependence between assets within the same postcode. This allows for the construction of an aggregated impact distribution at postcode level, from which the SCR is derived as the 99.5% Value-at-Risk (VaR), in line with Solvency II standards.

This approach provides a more realistic representation of loss concentration under extreme scenarios, avoiding simplifications that may underestimate aggregated risk in portfolios exposed to fluvial flooding.

| Postcode | District | Δ SCR |

| 41011 | Los Remedios | +6.03% |

| 41015 | Distrito Norte | +0.00% |

| 41010 | Triana | +11.22% |

| 41008 | Macarena | +52.99% |

| 41003 | Casco Antiguo | +166.27% |

SCR variation between baseline historical data and an unfavourable scenario up to 2035 among the five most exposed postcodes in Seville.

Once again, the historic centre and the Macarena district stand out not only due to their current exposure levels, but also because of the significant increase in expected risk over the next decade under an adverse scenario. This illustrates how a forward-looking view of hazard can materially change risk assessment compared to an approach based solely on historical data.

The analysis also identifies other postcodes which, while not among the most exposed in absolute terms, show a high sensitivity to climate change. This is the case for areas such as La Buhaira and San Pablo–Santa Justa, where exposure to fluvial flood risk could increase significantly (in some cases by up to 65%) compared to a historical baseline.

Overall, these results reinforce the need to complement traditional approaches with more granular and forward-looking analysis, capable of capturing both the current concentration of exposure and its potential evolution under different climate scenarios.

The insurance gap and the Spanish Consorcio de Compensación de Seguros

The Spanish insurance market has a distinctive feature: the existence of the Consorcio de Compensación de Seguros (CCS), Spain’s public insurance compensation scheme. In the case of fluvial flooding, these events are classified as extraordinary risks, meaning that the Consorcio (rather than private insurers) is responsible for compensating damages, provided that a valid insurance policy is in place within the relevant lines of business.

This public-private arrangement adds an additional layer of protection and diversification against natural disasters and enhances the overall resilience of the system. However, it does not eliminate one of the key concerns identified by both national and European supervisors: the insurance gap.

The insurance gap is not limited to the absence of coverage for exposed assets. It also includes situations where existing protection is insufficient or does not adequately reflect the underlying risk. This can occur when physical risk evolves faster than models based on historical data, when exposure is not properly located, or when certain losses fall outside the effective scope of coverage.

In this context, even in a system like Spain’s, the insurance gap can persist for several reasons: uninsured assets, policies that do not fully cover the risk, or an incomplete understanding of the true exposure profile within insurance portfolios. Moreover, the Consorcio mechanism itself requires the existence of a prior policy, meaning that part of the exposure may remain outside the protection system if it is not insured in the first place.

For this reason, the presence of the CCS does not remove the challenge, it reshapes it. Physical climate risk continues to pose a shared challenge for both supervisors and insurers: how to properly measure the evolution of risk, how to reflect it in underwriting and portfolio management, and how to avoid a scenario in which increasing severity, frequency and concentration of exposure translate into affordability pressures or even insurability constraints in certain areas.

Ultimately, reducing the insurance gap is not only about extending coverage, but about improving how risk is measured and understood. Incorporating a forward-looking view of hazard and a more granular representation of exposure allows insurers to make more informed decisions, anticipate potential portfolio tensions, and contribute to a more resilient insurance system in the face of physical climate risks.

Contents

Want to discuss climate risk for your insurance portfolio? Let's talk.

At Alpha-Klima, we help insurers turn physical climate risk into traceable, portfolio-relevant analysis by linking hazard, vulnerability, impact and aggregation into outputs that support underwriting, risk management and reporting.