Alpha-Klima helps institutions navigate complex climate and sustainability regulations by translating regulatory requirements into structured, auditable, and decision-ready outputs aligned with leading frameworks.

Ensure consistency with key climate and sustainability regulations, including CSRD, EU Taxonomy, and banking supervisory expectations.

Simplify complex regulatory requirements by converting data, models, and scenarios into clear, standardized disclosures.

Reduce regulatory risk by delivering transparent, traceable outputs designed for supervisory review and external audits.

A structured approach that maps climate risk data and metrics directly to regulatory requirements and reporting standards.

Generate consistent, comparable disclosures aligned with regulatory templates and supervisory guidance.

Full transparency from data sources to final outputs, supporting internal controls and audit processes.

Bridge risk, finance, sustainability, and compliance teams with a single, coherent regulatory view.

Built to support evolving regulatory frameworks, translating climate risk analysis into compliant disclosures and supervisory-ready documentation.

Robust internal controls and validation processes ensure consistency, accuracy, and regulatory alignment across climate risk analyses and disclosures.

End-to-end traceability from source data to reported outputs enables efficient audits, supervisory review, and full methodological transparency.

Clear ownership, documented methodologies, and defined responsibilities support strong regulatory governance and accountability across teams.

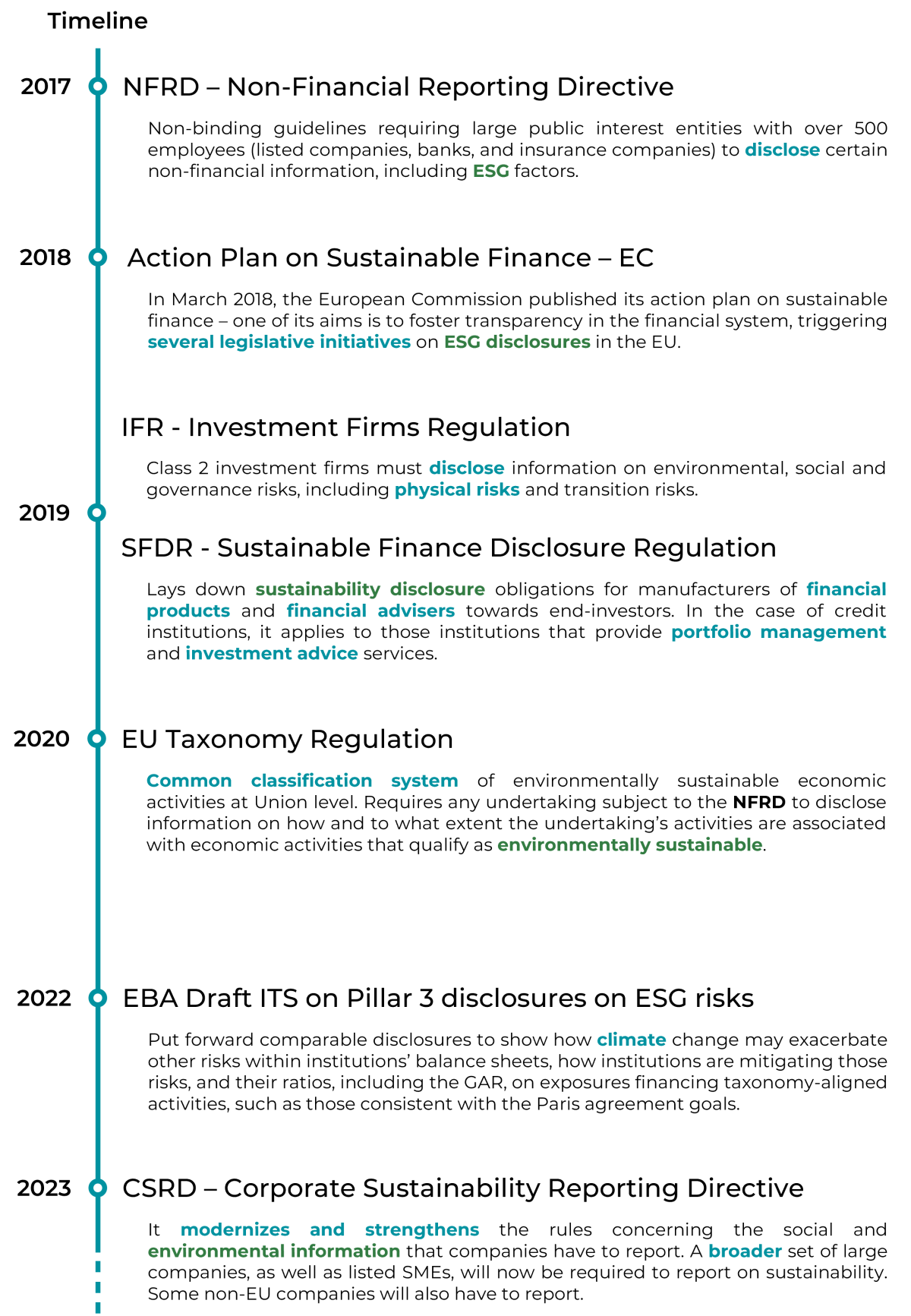

The European Union has recognized the critical need for robust climate risk assessment and effective adaptation strategies. In March 2018, the European Commission published an Action Plan to foster a sustainable financial system, with a strong emphasis on integrating Environmental, Social, and Governance (ESG) guidelines. The Plan aims to integrate sustainability into risk management and enhance transparency on sustainability-related issues, requiring new reporting obligations and data collection efforts. Strengthening resilience and reducing vulnerability to climate change are also key components of the European Climate Law and the EU Strategy on Adaptation to Climate Change.

Commission Implementing Regulation (EU) 2022/2453

Most banks subject to the EU’s CRD IV/CRR. Including large EU institutions under the supervision of the ECB, or those with securities traded on a regulated market of any EU member state.

“Large” = any bank with assets exceeding €30 billion.

Template 5 provides information on exposures in the banking book (loans and advances, debt securities and equity instruments not held for trading and not held for sale) towards non-financial corporates, on loans collateralised with immovable property and on repossessed real estate collateral. These exposures are segregated by:

Commission Delegated Regulation (EU) 2023/2772 — see also the Q&A on the Adoption of ESRS

| Entity Type | Fiscal Year | Starts Reporting in |

|---|---|---|

| Entities already subject to NFRD (large listed companies, large banks and large insurance undertakings — all if > 500 employees) | 2024 | 2025 |

| Large undertakings* not currently subject to NFRD | 2025 | 2026 |

| SMEs with listed securities (excluding micro-undertakings*) | 2026 | 2027 |

| Third-country undertakings* | 2028 | 2029 |

* see “Who is affected” criteria above.

The European Sustainability Reporting Standards (ESRS) are mandatory for use by companies obliged by the Accounting Directive to report sustainability information. The Accounting Directive, as amended by the CSRD in 2022, ensures companies across the EU report comparable and reliable sustainability information.

The ESRS take a double materiality perspective — companies must report both:

Out of the 12 topical ESRS proposed by EFRAG, the European Commission has decided that all reporting requirements should be subject to materiality, with the exception of ESRS 2 — General Disclosures. This includes also ESRS E1 — Climate Change.

ESRS E1-9 is consistent with Commission Implementing Regulation (EU) 2022/2453 — Template 5 discussed in Pillar 3 above.

| Step | Component | Description | Example assessment |

|---|---|---|---|

| 1 | Identify Potential Physical Risks | Use data on extreme weather, climate projections, and asset locations to identify high-risk areas. | Coastal assets identified as vulnerable to sea-level rise and tropical storms. |

| 2 | Assess Impact Materiality | Evaluate if physical risks could significantly affect people or the environment (scale, scope, irremediable character). | Scale: 20% of assets in high-impact zones. Scope: tenant displacement and major environmental repair costs. Irremediable Character: High (flood-prone areas may incur unrecoverable damages). |

| 3 | Assess Financial Materiality | Quantitatively model financial impacts: lost revenue, repair costs, insurance premiums. | Estimated repair costs for flooding: €10M/year. Projected insurance premium increase: 15% over 5 years. Scenario (2 °C warming): 10% reduction in asset value. |

| 4 | Scenario Analysis | Test physical risk impacts under 1.5 °C, 2 °C, or 4 °C warming. | Under 2 °C, projected annual revenue at risk: €8M. |

| 5 | Stakeholder Impact and Engagement | Identify stakeholders impacted: tenants, investors, regulators. | High concern from tenants on asset reliability — additional disclosures and adaptation investments required. |

GreenBuild Corp determines physical climate risks are material due to:

GreenBuild Corp would report:

Get in touch with our team — we deliver Pillar 3 Template 5 and CSRD ESRS E1-9 outputs end-to-end, with audit-ready documentation.